Origins: Who Invented Money - And Why It Wasn't Barter

Who invented money? The barter story is wrong. Debt and credit came first, coins arrived later, and Lydian electrum stamps solved the trust problem around 600 BC.

The standard origin story of money runs as follows: early humans bartered, trading two chickens for one clay pot, and the inefficiency of this arrangement eventually drove them to invent a medium of exchange. Coins arrived, then paper money, then credit cards, and here we are.

This story is wrong. Not approximately wrong, or wrong in minor details, but fundamentally wrong in its sequence and its evidence base. The barter economy that supposedly preceded money has never been documented anywhere by any anthropologist. The sequence runs in the opposite direction. Money did not replace barter. Money replaced debt.

The barter myth and where it came from

Adam Smith introduced the barter-to-money sequence in "The Wealth of Nations" in 1776, as a logical deduction from first principles. If money is useful, he reasoned, then its absence must have been inconvenient, and the inconvenience of barter must have driven its invention. This is elegant theory. It is not observation of any actual human society.

When anthropologists examined the ethnographic record for examples of barter economies - communities where people regularly exchanged goods with strangers in the absence of any monetary medium - they found isolated instances, but a systematic pattern. Barter, when it did occur, happened between communities that did not trust each other, often in the context of trade with outsiders. Within communities, the dominant mode of organizing exchange was something else entirely: reciprocal gift-giving, communal sharing, and credit.

David Graeber, an anthropologist at the London School of Economics, assembled the most comprehensive critique of the barter myth in his 2011 book "Debt: The First 5,000 Years." His central argument, drawing on decades of anthropological fieldwork and historical scholarship, is that credit and debt - the acknowledgment that one party owes something to another - are the oldest form of economic organization that we have good evidence for. Money, in the sense of a physical medium of exchange, came later, and came partly as a way to resolve and discharge debts rather than to replace barter.

Mesopotamia: accounting before coins

The oldest physical evidence of monetary reckoning comes from Mesopotamia, the civilization that developed in the river valleys of modern Iraq. Clay tablets from Sumerian cities, dating to roughly 3000 BC or somewhat earlier, record debts in units of silver by weight. The shekel was originally a unit of weight - about 8.33 grams - not a coin. No coin existed yet. The tablet recorded what was owed, to whom, for what, and by when.

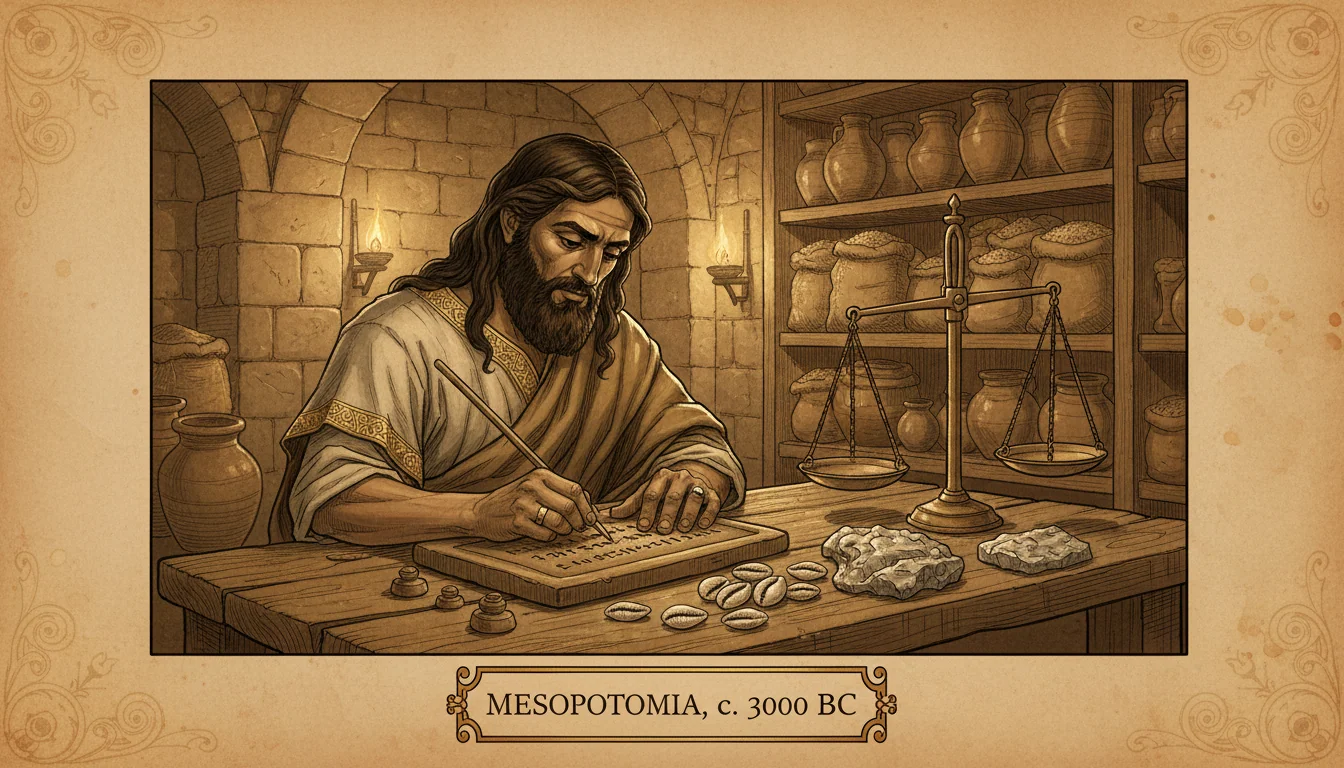

The Sumerian temple was the economic center of these early cities. Temples received grain and labor as tribute, stored it, processed it into bread and beer, and redistributed it to temple workers and craftspeople. The system created massive flows of goods and labor organized not by market exchange but by centralized administration. Within this system, silver by weight served as the unit of account for larger transfers: a farmer's annual tithe, a merchant's trading advance, a craftsman's long-term contract.

Interest was charged on these early loans - the Sumerian word for interest, "mas," also meant the offspring of an animal, a productive yield. The concept that money lent should generate more money returned is ancient. The debate about whether this was appropriate is equally ancient; the later religious prohibitions on usury in Jewish, Christian, and Islamic law were responding to a practice at least three thousand years old.

The key point is that the shekel preceded any coin by roughly two millennia. Money as a unit of account, a way of measuring what is owed, came long before money as a physical object you could hold in your hand.

Commodity money: shells, grain, and copper

Independently of Mesopotamian silver accounting, various cultures developed commodity money - standardized physical objects that served as a medium of exchange because their properties made them convenient: durable, portable, divisible, and difficult to counterfeit.

Cowrie shells, specifically the shells of the Monetaria moneta species, served as currency across an extraordinary geographic range. Archaeological evidence shows cowrie use as currency in China from at least the Shang dynasty, roughly 1500 BC, with possible earlier use. The shells circulated in coastal and inland South Asia, across much of sub-Saharan Africa, and in parts of Southeast Asia. Their appeal was practical: they are visually distinctive, difficult to fake with natural materials, uniform enough in size to function as units, and durable enough to last in storage.

The Chinese character for "money" - bei - is a stylized cowrie shell. The characters for "buy," "sell," "wealth," "treasure," and "goods" all contain this element. The shell was so fundamental to early Chinese economic vocabulary that its image became embedded in the language itself.

In ancient Egypt, the dominant forms of commodity exchange used grain, copper, and gold and silver by weight. Egypt did not adopt coinage from Greece until the late period, well into the first millennium BC. For much of its three-thousand-year history, Egyptian economic life ran on rations, weight-measured metals, and a sophisticated system of state redistribution through the granary network.

Lydia and the first coins

The technological leap that produced coinage - as distinct from commodity money - was the state guarantee of weight and purity. A merchant receiving silver by weight had to weigh it and assess its purity at every transaction. This introduced friction and opportunities for fraud. A coin stamped with a royal seal solved both problems: the issuing authority guaranteed that the lump of metal weighed a specific amount and contained a specific proportion of valuable metal.

This innovation appeared in Lydia, a kingdom in western Anatolia - modern western Turkey - in approximately 650-600 BC. The precise date is disputed; the earliest Lydian coins are typically attributed to the reign of King Alyattes, with a slightly later refining of the system under his son Croesus. What made Lydia's geography relevant was the Pactolus River, which ran through the royal capital of Sardis and carried deposits of electrum, a naturally occurring alloy of gold and silver. The Lydian hills were, in the literal ancient sense, worth mining.

The early Lydian coins were made of electrum and stamped with a lion's head - the symbol of the Lydian royal house. The stamp was the critical element. It meant you did not have to test every coin. You trusted the royal guarantee.

Croesus, who has given us the phrase "rich as Croesus," took the system further by introducing separate pure gold and pure silver coins, abandoning the mixed electrum. This bimetallic system allowed more flexible pricing and exchange and became the model that Greek city-states rapidly adopted.

The Greek and Persian spread

Greek traders encountered Lydian coinage through commercial contact across the Aegean and adopted it with remarkable speed. Within roughly a century of the Lydian invention, dozens of Greek city-states were minting their own coins. The Athenian tetradrachm, bearing the owl of Athena, became a widely recognized trade coin across the Mediterranean. The Corinthian stater, the Aeginetan turtle - each city-state's coin was its signature.

The Achaemenid Persian Empire, which absorbed Lydia after Cyrus the Great's conquest of Sardis around 547 BC, issued its own coinage: the gold daric (bearing the image of the archer-king) and the silver siglos. Persian coinage circulated across an empire stretching from the Aegean to India, and the standardization of currency across this vast area represented a genuine administrative achievement.

Alexander the Great's conquests in the 330s to 320s BC redistributed enormous quantities of Persian and Lydian treasury metal - billions of drachmas worth - into circulation across the Mediterranean and Near East. This was not just military history; it was a monetary event. The sudden availability of coined metal at scale accelerated trade and commercial activity across the Hellenistic world.

China's independent invention

At roughly the same period - and without apparent connection to Lydian or Greek development - China was developing its own tradition of metal currency. Bronze implements shaped like spades and knives had been used as commodity money during the Zhou dynasty, their value derived from the underlying metal and their function as recognizable objects of trade. By the Warring States period (475-221 BC), these had begun to be miniaturized and stylized into tokens that represented the object rather than serving as actual tools.

Qin Shi Huang, the first emperor who unified China in 221 BC, standardized the currency as round coins with square holes - a form that would persist with remarkable consistency for two thousand years. The round form represented heaven; the square hole represented earth. The holes allowed coins to be threaded on strings for carrying and counting.

The gap between the story and the archaeology

What the physical and documentary record shows, then, is a sequence quite unlike the textbook version. Credit and debt accounting appeared in Mesopotamia around 3000 BC. Commodity money - shells, metal by weight, grain - circulated in various forms across many cultures through the second millennium BC. Coined money, with its state-guaranteed standard, appeared in Lydia around 650-600 BC and spread through the Aegean and then the Mediterranean world within a few centuries.

At no stage in this sequence does a barter economy appear as the precursor. The communities that first developed monetary instruments were not primitive traders frustrated by the limits of barter. They were sophisticated administrative societies that needed better ways to record and transfer obligations: temple economies, palace economies, long-distance trading networks organized by credit.

Adam Smith's theoretical barter-to-money story was an attempt to explain money from first principles, without the archaeological evidence that would accumulate over the following two centuries. It was a reasonable speculation given what he knew. What the archaeology has since shown is that human beings, given the choice between trading two chickens for a clay pot face to face or agreeing that one party owes the other a clay pot to be settled at the next harvest, consistently chose the second option first.

Money followed because debt is harder to store than a coin.

For related origins histories, see Origins: Who Invented the Stock Market? and Origins: Who Invented the Bank?.

Quick Answers

Common questions about this topic

Who invented money?

No single person or civilization invented money, but the earliest documented evidence of formalized monetary systems points to Mesopotamia around 3000 BC, where temple administrators recorded debts in silver by weight. The first true stamped coins - the innovation that guaranteed a unit's weight and purity by state authority - appeared in Lydia (modern western Turkey) around 650-600 BC, probably under King Alyattes.

Did humans really use barter before money?

There is no documented evidence that any society organized itself primarily around barter before developing credit and money. The barter-precedes-money narrative was a theoretical construct by Adam Smith in 1776, not an observation of any actual society. Anthropologists and economic historians, most prominently David Graeber in his 2011 work Debt: The First 5,000 Years, have found that credit, gift economies, and centralized redistribution preceded commodity exchange as the dominant modes of economic organization.

Why did Lydia invent coinage?

The Lydian kingdom in western Anatolia sat on deposits of electrum, a naturally occurring gold-silver alloy found in the Pactolus River. Lydian rulers solved a persistent problem: trading partners had to verify the purity and weight of every metal payment they received. A state-stamped coin bearing the royal seal guaranteed both. This reduced transaction costs and made exchange faster and more reliable, driving adoption across the Greek world within a generation.

What were the earliest forms of money?

The earliest well-documented monetary instruments are clay tablets from Mesopotamia recording debts - what someone owed, to whom, and when. Commodity money - using standardized objects as a medium of exchange - appeared in various forms: cowrie shells across China, South Asia, and Africa; silver by weight in Mesopotamia; grain and copper in Egypt. None of these were 'invented' at a single moment; they emerged gradually as societies needed reliable ways to represent and transfer obligation.

Never miss a mystery

Get new investigations in your inbox

Weekly deep-dives on unsolved cases, Hollywood vs. history, and ancient civilizations. No spam. Unsubscribe anytime.