Origins: How Insurance Was Invented

The origins of insurance trace to Babylonian merchants in 1750 BC, Genoese traders in the 1300s, and a London coffee house that became Lloyd's.

The first time a human being transferred financial risk to someone else in exchange for a payment, there was no word for what had been done. The concept was probably older than the vocabulary available to describe it: someone has a voyage to make, the voyage might kill them and their capital together, and somewhere another person decides that a smaller certain payment now is worth the chance of a larger uncertain payout later if disaster strikes.

That logic is at least 3,700 years old. The institution it produced has outlasted empires, survived repeated bans, burned down cities and then insured the rebuilding of them, and become one of the largest industries in the global economy. Its origins are not at Lloyd's of London, and they are not in Renaissance Genoa. They are in a cuneiform tablet from Mesopotamia where a merchant and a lender argue about who owes what if the ship does not come back.

Babylon and the bottomry loan

The Code of Hammurabi, promulgated by the Babylonian king around 1750 BC, is best known for its retributive provisions. Less discussed but equally significant for economic history are its regulations governing bottomry loans - the financial instrument that is the direct ancestor of marine insurance.

A bottomry loan worked as follows. A merchant planning a sea voyage needed capital to buy cargo. A lender advanced that capital at a high interest rate - often 20 to 30 percent, far above rates for ordinary land loans, sometimes higher for especially dangerous routes. The critical clause was the disaster provision: if the ship sank, the merchant owed nothing. The entire loss was the lender's to bear.

The lender was not being charitable. The interest rate on a successful voyage more than compensated for the risk of an unsuccessful one, provided the lender distributed loans across enough voyages. This is precisely the actuarial logic of a modern insurance pool: many successful small premiums collectively absorb the large payouts from the rare disasters.

Bottomry loans appear in Mesopotamian, Greek, and Roman sources spanning more than two thousand years. By the classical Greek period, Athenian bottomry was a specialized financial market with its own legal vocabulary and professional operators. Demosthenes, in his courtroom speeches of the 4th century BC, describes bottomry disputes in enough detail to reconstruct the standard contract terms. The Romans called the instrument foenus nauticum - "nautical interest" - and their legal codes specified exactly when the disaster clause applied and what evidence a borrower had to produce to avoid repayment.

The bottomry loan was not insurance in the modern sense - the risk was bundled with the loan rather than sold as a separate product - but the economic function was identical. A merchant who paid 30 percent on a loan forgiven if the ship sank was buying protection against catastrophic loss at a calculable premium.

Genoa, 1347: the first written contract

The transition from embedded risk-transfer to standalone insurance contract happened in the Italian city-states in the 14th century, where the volume and complexity of Mediterranean trade demanded more flexible instruments than a combined loan-and-coverage arrangement.

The earliest surviving written insurance contract in the world is a Genoese notarial document dated October 23, 1347. It covers a ship named the Santa Clara on a voyage from Genoa to Majorca. A group of underwriters agreed to pay a specified sum if the vessel was lost; in return they received a premium paid upfront by the merchant. The bottomry structure is absent. This is a pure insurance contract: a premium paid now, coverage provided in exchange, nothing else.

Several hundred similar contracts survive from Genoa and Venice in the second half of the 14th century. By the 1390s, Florentine and Venetian merchants were writing policies on inland cargo as well as sea voyages. Specialized insurance brokers - distinct from both the shippers and the underwriters - appear in the records by the early 15th century. The commercial insurance market was fully functional in northern Italy before 1400.

Genoa also produced, in 1435, one of the first commercial codes to specifically regulate insurance: the Ordinamenta et consuetudo maris, which established rules for policy wording, premium payment, and dispute resolution. By the mid-15th century, Barcelona had its own insurance regulations. The Hanseatic trading cities of northern Europe were importing the practice from their Mediterranean partners within another generation.

The Great Fire and property insurance

Marine insurance covered ships. It said nothing about houses.

The Great Fire of London in September 1666 destroyed roughly 13,200 houses and 87 churches across 373 acres of the city's commercial core. The economic shock created a demand that had never existed before: coverage against the loss of a building. Within fifteen years, a property developer named Nicholas Barbon had founded the first fire insurance office in London. His Fire Office, established in 1681, employed its own brigade of firefighters who were dispatched only to buildings displaying the company's metal fire mark - a small plaque affixed to the facade of insured properties.

If your house was burning and did not display the correct mark, the brigade watched from a safe distance.

Barbon's venture attracted competitors quickly. The Hand in Hand (1696) and the Sun Fire Office (1710) were among the early followers. By the early 18th century, property insurance was available to London homeowners and spreading to the provinces. The fire mark on a building's facade - indicating which insurer had the coverage and would dispatch the brigade - became a fixture of English urban architecture for over a century.

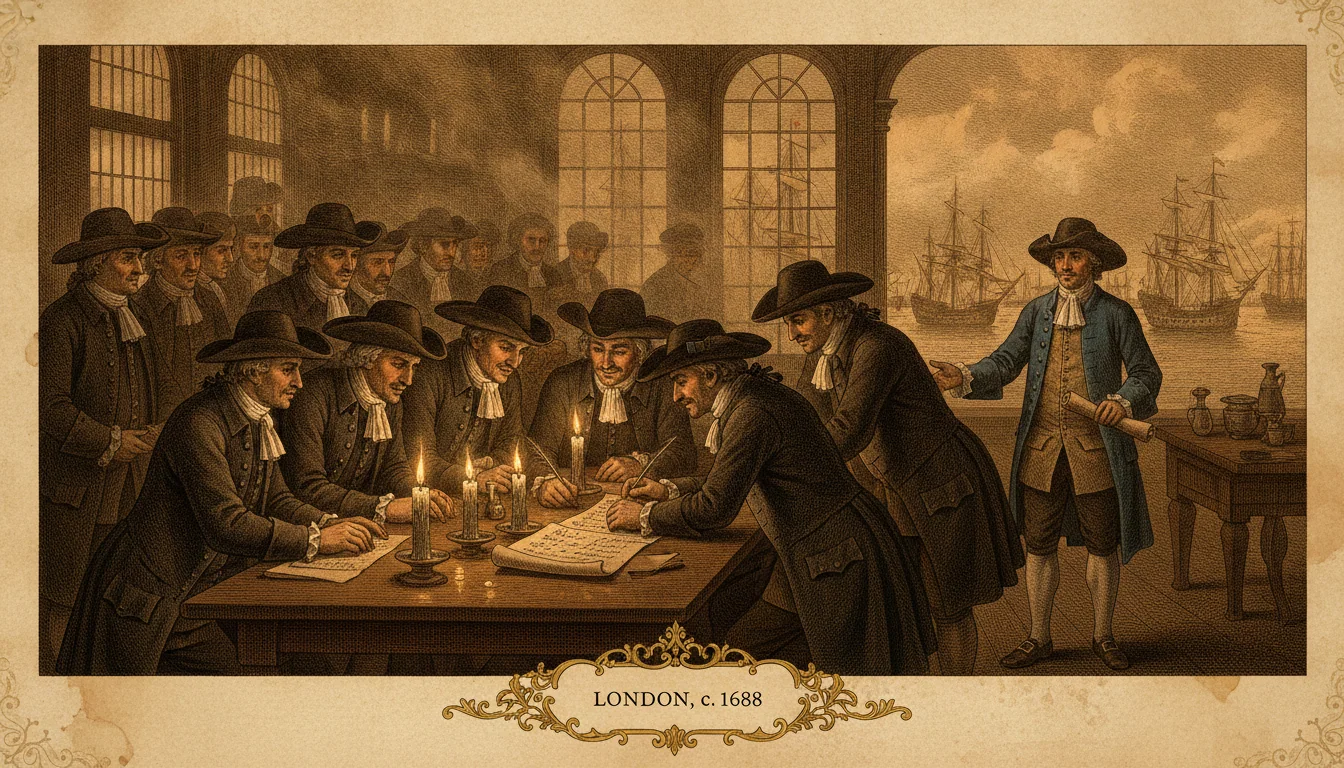

Lloyd's coffee house

Around 1688, a man named Edward Lloyd opened a coffee house on Tower Street in London, near the Royal Exchange and the Custom House, at the geographic heart of the city's shipping district.

Lloyd was not an underwriter and did not sell insurance himself. He was a coffee-house keeper whose specific clientele - merchants, shipowners, sea captains, and speculators willing to bet on whether a given vessel would survive a given voyage - found his premises useful. Lloyd kept shipping intelligence, maintained a register of vessels and their reported conditions, and circulated handwritten news sheets with information his customers valued.

The practice that developed at his tables was informal but precise. A merchant seeking coverage on a voyage would circulate a slip of paper describing the ship, the cargo, the destination, and the sum to be covered. Willing underwriters would write their name under the risk description and the percentage of the exposure they were willing to accept - which is exactly where the word "underwriter" originates. A slip might pass through a dozen hands, each accepting a fraction, until the full sum was subscribed.

This syndicate model - spreading risk across many underwriters rather than concentrating it in a single insurer - is still the operational basis of Lloyd's of London. The corporate institution that replaced the coffee house was incorporated in 1871, but the fundamental mechanism has not changed: a slip of paper circulates, and names go on the bottom.

The actuarial breakthrough

Insurance markets can function without actuarial science - bottomry lenders priced intuitively from route knowledge and accumulated experience - but they price risk far more accurately with it.

The intellectual turning point came in 1693, when Edmond Halley - the astronomer whose name attaches to the comet - published a mortality table based on the detailed birth and death records of the Silesian city of Breslau. Halley was not primarily interested in insurance: he was interested in the mathematics of human survival probability for its own sake. But his table, the first rigorous mortality analysis in European scientific literature, gave life insurers a tool they had never possessed: a calculation of how long a person of a given age could statistically be expected to live.

The first formal life insurance company in England, the Amicable Society for a Perpetual Assurance Office, was founded in 1706. By the mid-18th century, actuaries who could work with Halley's tables and their successors were pricing annuities, life policies, and increasingly complex financial instruments across the European insurance market.

The popular myth and the actual sequence

The popular story places insurance's invention at Lloyd's of London in the late 17th century, as if the English improvised risk-sharing from scratch over coffee. The actual sequence is longer and more crowded: bottomry loans in Babylon and classical Athens, formalized maritime contracts in medieval Genoa, property coverage after the London fire, life insurance in the 18th century, and Lloyd's as the clearinghouse that happened to be present at several of these steps and lent its name to one of them.

What unifies the sequence is a single observation that appears to be universal across complex economies: some losses are too large for one person to absorb alone, and it is possible to pool many small certain payments to cover the few large uncertain ones. The mathematics for doing this well - actuarial science, probability theory, mortality tables - took millennia to develop. The underlying social contract did not wait for the mathematics.

A Babylonian lender writing a bottomry clause into a clay tablet in 1750 BC and an underwriter at Lloyd's scrawling his name under a shipping risk in 1700 AD were separated by 3,400 years of history and doing the same thing. The forms changed entirely. The logic did not change at all.

The next time someone suggests that insurance is a modern financial invention, you can answer that it predates both coined money and the Roman Empire, and that the Hammurabi Code's provisions for shipping losses were more clearly written than most standard-form policies in use today.

The origins of insurance are part of a broader story about how humans invented institutions to manage collective risk. For related histories of financial infrastructure, see the origins of banking and the origins of money.

Quick Answers

Common questions about this topic

When was insurance invented?

The concept of transferring financial risk appears at least as far back as ancient Babylon. The Code of Hammurabi (c. 1750 BC) contains provisions for bottomry loans, in which a merchant borrowed money for a sea voyage and owed nothing if the ship sank. Formal written insurance contracts appeared in Genoa in 1347. Lloyd's of London, the institution most people associate with insurance, traces to a coffee house opened around 1688.

What was a bottomry loan?

A bottomry loan was a financial instrument used across the ancient Mediterranean world in which a lender advanced capital to a merchant before a sea voyage at a high interest rate - often 20 to 30 percent or more. The critical clause: if the ship was lost, the borrower owed nothing. The lender absorbed the loss entirely. This transferred catastrophic risk from the merchant to the lender, which is the core function of insurance, even though the risk was embedded in a loan rather than sold as a separate product.

What was the first written insurance policy?

The earliest known written insurance contract is a Genoese notarial document dated October 23, 1347, covering a ship named the Santa Clara on a voyage from Genoa to Majorca. Underwriters agreed to pay a specified sum if the vessel was lost, in exchange for a premium paid upfront. Unlike bottomry, this was a standalone insurance contract - the risk was separated from any loan and sold independently.

How did Lloyd's of London start?

Edward Lloyd opened a coffee house on Tower Street in London around 1688, near the Custom House and the Royal Exchange. It attracted merchants, shipowners, and speculators willing to underwrite marine voyages. Willing parties would sign their name beneath a risk description on a circulating slip of paper - which is where the term 'underwriter' comes from. Each signer accepted a share of the exposure. The Lloyd's market incorporated formally in 1871 but the syndicate model has not fundamentally changed.

Ask the Inventors Themselves

Chat with the people who were there when familiar things began.

Trace It to the Source