Origins: Where Paper Money Was Actually Invented

The origins of paper money trace to Song Dynasty China, where a government monopoly in Sichuan transformed private merchant notes into the world's first true currency.

The story that gets told in economics textbooks usually begins with a 9th-century Chinese merchant too burdened by copper coins to travel conveniently, who deposited his coins with a trusted agent and received a piece of paper acknowledging the debt. From there, the story runs, it was only a short step to paper money as we know it.

This narrative is not wrong. It is just too short by about two centuries and several institutional crises.

The actual origins of paper money were not a single moment of merchant ingenuity but a slow, contested, government-driven process that involved a copper shortage in Sichuan province, a series of private bank failures, a state monopoly enforced by bureaucratic fiat, and eventually the Mongol conquest of the entire apparatus and its expansion to the largest empire in the world. By the time Marco Polo encountered Chinese paper money in the 1270s and reported it with barely concealed amazement to European readers, what he was describing had taken three hundred years to develop from its earliest recognizable precursor.

Tang Dynasty flying money: the precursor that was not currency

The first piece of the story belongs to the Tang Dynasty (618-907 AD), and it concerns a problem that anyone who has tried to move large amounts of physical cash understands. Tang China used copper coins as its primary medium of exchange. A copper coin is heavy, bulky, and inconvenient to transport across hundreds of miles of mountain road. A merchant in the capital Chang'an who needed to pay a supplier in Guangzhou faced the practical difficulty of moving the equivalent weight in metal.

The Tang government and large merchant houses developed a partial solution called feiqian, meaning literally "flying money." A merchant could deposit coins with an agent in one city and receive a paper certificate, which could be redeemed at a corresponding office in another city. It was a bill of exchange, a formalized IOU backed by the depositor's coins sitting somewhere else.

This was not paper money. The state did not guarantee feiqian as payment for taxes or debts. There was no central authority behind the certificate beyond the creditworthiness of the particular merchant house that issued it. If that house failed, the certificate was worthless paper. The coins were still the real money; feiqian was a logistical convenience layered on top of them.

The Tang Dynasty understood the distinction and was cautious about blurring it. The government eventually moved to regulate the private feiqian system and establish its own "convenient money" offices, but it did not issue the certificates as legal tender. The step from convenience instrument to currency remained untaken.

Sichuan and the copper problem

The Song Dynasty, which reunified much of China after the chaotic Five Dynasties period (907-960 AD), inherited an empire with a structural monetary problem in its southwestern province of Sichuan. Sichuan used iron coins rather than the copper standard of most of China because the Yangtze River gorges made transporting copper into the province expensive. Iron coins were worth less per unit weight than copper, which meant that Sichuan commerce required very large volumes of very heavy coins for significant transactions.

Wealthy Sichuan merchants responded in the early 10th century by creating their own private paper instruments called jiaozi, meaning approximately "paper vouchers." A merchant could deposit iron coins with one of sixteen large Sichuan trading houses and receive a jiaozi in return, which other merchants would accept in commerce because they trusted the issuer's creditworthiness. These were still not government money. They were private bank notes backed by private iron coin reserves.

The system worked until it did not. Some of the issuing houses over-lent their reserves, issued more jiaozi than their coin holdings could support, and when depositors came to redeem them simultaneously, the houses could not pay. The resulting failures disrupted Sichuan commerce significantly and prompted demands for government intervention.

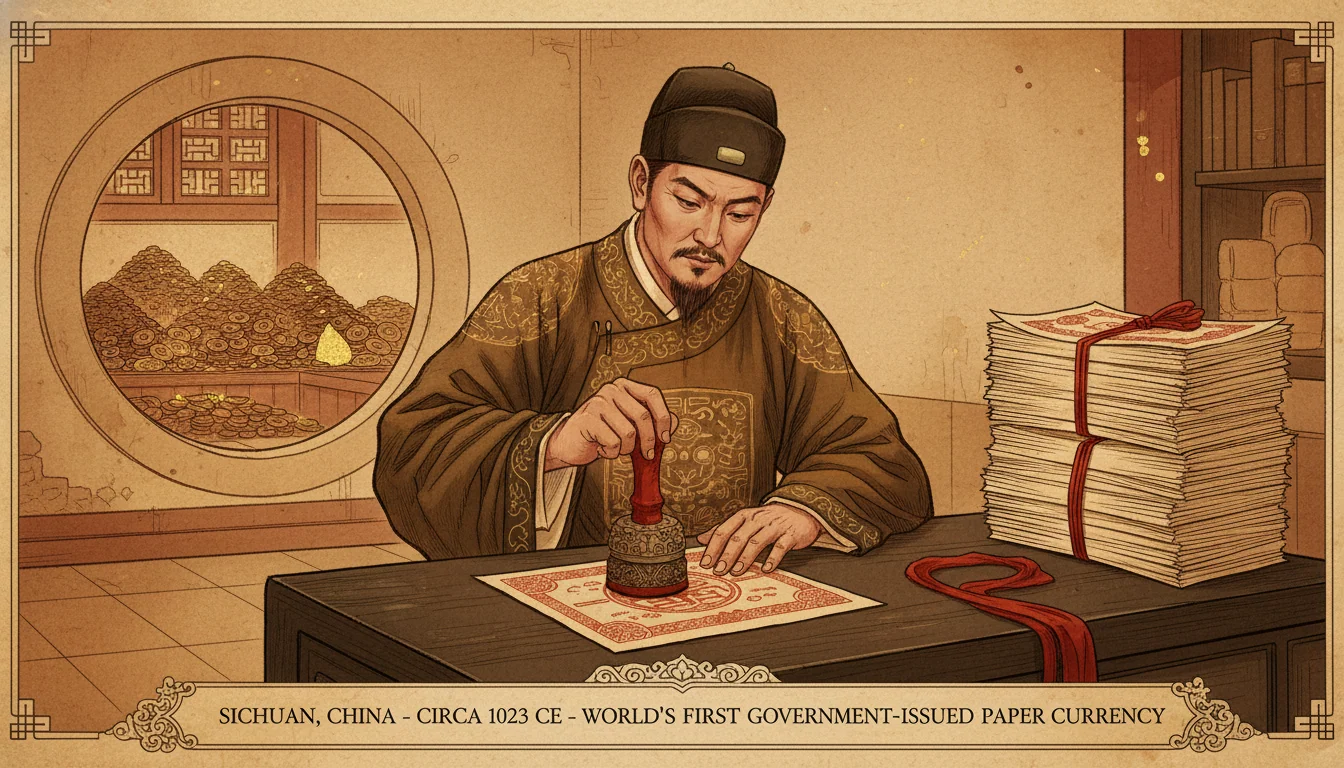

1023: the state steps in

The Northern Song government's response was decisive and represents the actual invention of paper money in the historical sense. In 1023 AD, the government of Emperor Renzong nationalized the jiaozi system in Sichuan, establishing a government office called the Jiaozi Office to issue and manage the notes. The government's notes were:

- Issued in standard denominations, from 1 to 10 strings of coins in equivalent value

- Backed by a reserve of iron coins held in the Jiaozi Office

- Accepted for payment of taxes to the Sichuan provincial government

- Renewable every three years with a small fee

The last two points are what distinguish jiaozi under government management from any previous paper instrument. Acceptance for tax payment means the government is using its sovereign authority to create demand for the notes: if you owe taxes to the state, and the state will accept its own notes in payment, then those notes have value anchored in law rather than just in merchant trust. The three-year renewal requirement with a fee was a monetary policy tool, crude but real, that encouraged circulation rather than hoarding.

For the first time, paper itself was money - not a receipt for money held elsewhere, but an instrument that the sovereign required its subjects to accept.

Song monetary policy: sophistication and overreach

The Song government's management of paper currency over the following two centuries displayed both genuine sophistication and the characteristic failure mode of all unconstrained currency issuers. The Jiaozi Office maintained reserves, limited circulation to what its models suggested the Sichuan economy required, and adjusted supply in response to price signals. Song economic officials developed concepts that would not reach European economic theory for another six hundred years.

They also, when military emergencies arose, discovered that paper money was easier to print than to fund through taxation. The wars of the 12th century against the Jurchen Jin Dynasty, which captured the Song capital of Kaifeng in 1127 and forced the dynasty to reconstitute itself in the south as the Southern Song, strained fiscal resources catastrophically. Government note issuance expanded faster than reserves. Inflation followed. The sophisticated administrative system that had maintained the currency's credibility began to erode under the pressure of war finance.

The pattern - responsible management followed by emergency over-issuance followed by inflation - repeated across the Song and Yuan dynasties. It is the same pattern that has afflicted every government currency in every era since, and the Song were working through it for the first time without any institutional memory or theoretical framework to guide them.

Marco Polo and the Yuan

The Mongol Yuan Dynasty, which completed its conquest of China in 1279 under Kublai Khan, inherited the Song paper money system and expanded it aggressively. Kublai issued a single national paper currency, the jiaochao, and declared it legal tender throughout the empire. Existing metal coinage was demonetized and required to be exchanged for paper. The penalty for refusing jiaochao in commercial transactions was severe.

This was when Marco Polo encountered it, probably between 1275 and 1292. His description in The Travels is one of the most vivid accounts of genuine astonishment in medieval literature. He understood immediately that he was looking at something that had no equivalent in Europe. He noted the mulberry bark paper, the red ink seal, the official signatures, the requirement that all merchants accept notes on pain of death. He described Kublai's effective ability to manufacture wealth at will: the emperor's treasury could produce unlimited notes at the cost of the paper, while European kings spent fortunes melting and minting coin.

What Polo did not fully report, because his hosts did not emphasize it, was the inflation that periodically destroyed the Yuan paper currency's value. The structural problem of easy money creation versus disciplined reserve management, which the Song had struggled with, the Mongols solved less elegantly, largely by issuing new currencies and requiring old ones to be exchanged at disadvantageous rates.

Europe's much later arrival

European paper money arrived in 1661, when Johan Palmstruch at Sweden's Stockholm Banco issued Kreditivsedlar, credit notes that circulated as payment instruments. The Bank of England followed in 1694 with Exchequer bills. Both institutions were, without acknowledging it, reinventing a wheel that had been spinning in China for six centuries.

The European notes were initially fully convertible to gold or silver on demand, which made them effectively safer than the late Song and Yuan instruments but also limited their flexibility. The transition to fiat currency, paper backed only by government authority rather than metal reserves, did not complete in major Western economies until the 20th century. The United States formally ended gold convertibility for domestic purposes in 1933 and for international purposes in 1971.

The Tang merchants who first used feiqian to avoid carrying coins over mountain passes were solving a logistical problem. The Song bureaucrats who nationalized the jiaozi and made them legal tender were solving a monetary problem and in doing so created an institutional framework that shaped every government currency issued since. The mechanism of that creation, sovereign guarantee plus tax acceptance plus reserve management, is exactly what sits behind the paper or digital money in your wallet today.

The mulberry bark is gone. The logic is the same. For other Chinese inventions that transformed the world, see the histories of the printing press and gunpowder.

Quick Answers

Common questions about this topic

When was paper money invented?

True paper money - government-issued currency that citizens were required to accept as payment - was first issued in Sichuan province, China, during the Northern Song Dynasty around 1023 AD, when the government nationalized and standardized what had started as private merchant promissory notes called jiaozi.

What were flying money and jiaozi?

Flying money (feiqian) was a Tang Dynasty certificate system used by merchants to avoid carrying heavy copper coins over long distances. It was a bill of exchange, not currency: the state did not guarantee it as payment for debts. Jiaozi began as private promissory notes issued by wealthy Sichuan merchants in the early 10th century and were later nationalized by the Song government as the world's first true paper currency.

What did Marco Polo say about paper money?

Marco Polo visited China under Kublai Khan in the late 13th century and described the Yuan Dynasty's use of paper money with astonishment. He wrote that the Khan issued paper notes sealed with his seal, that all merchants across his territory were required to accept them, and that anyone refusing to do so faced the death penalty. He noted that the paper was made from the bark of mulberry trees and called the system more effective than any he had seen in the West.

When did paper money reach Europe?

European paper money arrived relatively late. Sweden's Stockholm Banco issued banknotes in 1661, generally cited as the first European paper currency. England followed with Bank of England notes from 1694. These were initially convertible receipts backed by gold deposits, not fiat currency. True fiat paper money, unbacked by metal, did not become standard in Europe until the 19th and 20th centuries.

Ask the Inventors Themselves

Chat with the people who were there when familiar things began.

Trace It to the Source